Every year, over 100 million Americans carry $195 billion in medical debt. Many don’t realize how easily a routine hospital visit can turn into a financial trap-especially when providers push credit cards or bundle consent forms without clear explanations. In 2024, New York State changed the game. Three new laws went into effect on October 20, 2024, giving patients real power over how their medical care is paid for and what they agree to. These aren’t just paperwork updates. They’re legal shields against predatory billing practices that have haunted families for decades.

Separate Consent for Treatment and Payment

For years, patients signed one form at the front desk-checking a box that gave consent for both medical treatment and payment collection. That’s over. New York’s Public Health Law Section 18-c now requires providers to get two separate signatures: one for care, one for payment. You can’t sign away your financial rights just because you’re filling out intake paperwork.

This matters because many patients didn’t even know they were agreeing to financing plans or credit card holds. Now, if a provider skips this step, they face a $2,000 fine per violation. The law is clear: your consent to get an MRI isn’t the same as your consent to pay for it with CareCredit or a credit card. You have to know what you’re signing.

But here’s the catch: as of August 2025, enforcement of Section 18-c has been suspended. That doesn’t mean the law is gone-it means providers are waiting for clearer guidance from the state. Until then, you should still ask for separate consent forms. If they refuse, you have the right to walk out and file a complaint with the New York State Department of Health.

No More Filling Out Your Credit Applications

Ever had a receptionist say, “I’ll just help you with this CareCredit form”? That’s illegal now. General Business Law Section 349-g bans healthcare staff from completing any part of a patient’s application for medical financing-no matter how helpful they seem.

Providers can answer questions. They can hand you the form. They can explain what CareCredit is. But they can’t touch the keyboard, fill in your income, or pre-check boxes. The application must be 100% your work. Why? Because if they help, they’re steering you toward a financial product they get paid to promote. And that’s a conflict of interest the law now blocks.

Violations come with a $5,000 fine per incident. That’s not a slap on the wrist. It’s a warning: don’t use patients as a sales channel.

Don’t Let Them Keep Your Credit Card on File

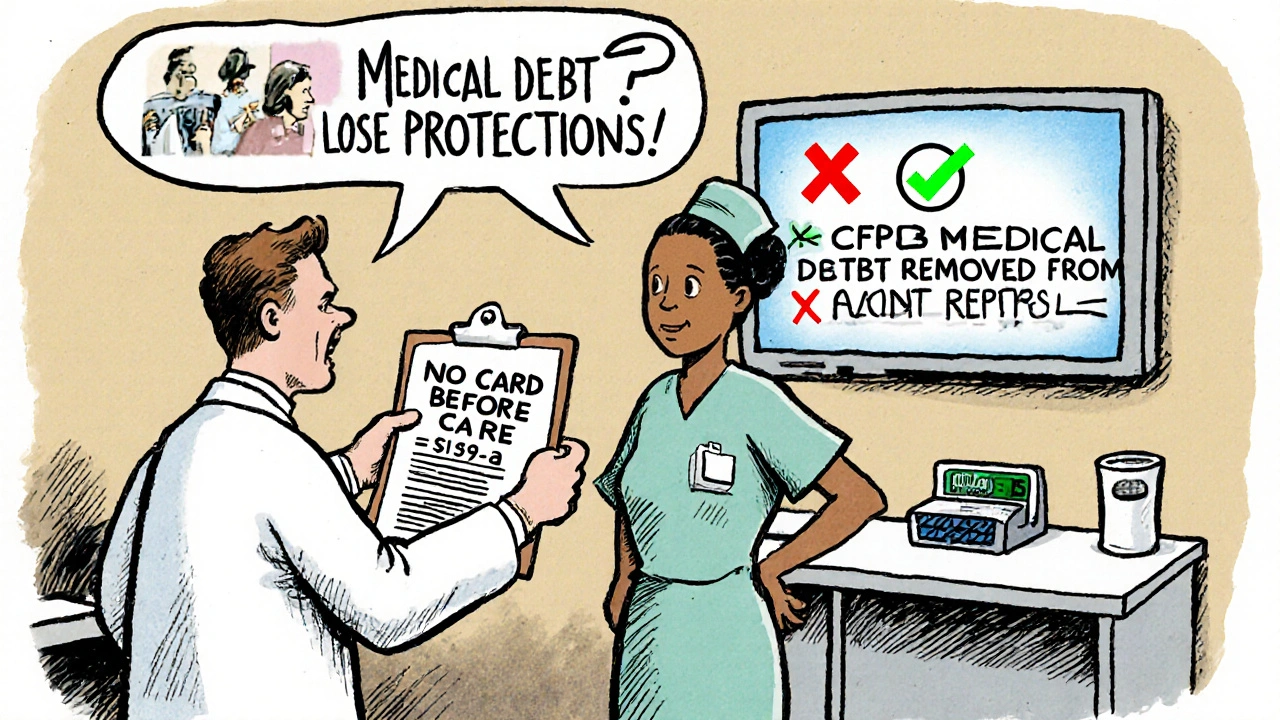

Emergency rooms used to ask for your credit card before they’d even look at your symptoms. That’s not just rude-it’s dangerous. General Business Law Section 519-a now makes it illegal to require a credit card preauthorization or keep your card on file before giving emergency or medically necessary care.

Providers must tell you, in writing, that paying with a regular credit card means you lose key protections. If you use a healthcare-specific financing plan like CareCredit, federal and state laws shield you from wage garnishment, liens on your home, and negative credit reporting. But if you just swipe your Visa? Those protections vanish. You’re treated like any other consumer debt-and that’s exactly what the law is trying to stop.

Every time you use a credit card for medical services, the provider must give you a clear notice: “Using a traditional credit card for this payment may expose you to collections, credit damage, and legal action. Healthcare financing products offer stronger protections.”

How This Compares to Federal Rules

The federal No Surprises Act, which started in 2022, stops surprise bills from out-of-network providers. That’s huge. But it doesn’t touch what happens inside the clinic. New York’s laws go further. They protect you from financial traps even when you’re seeing an in-network doctor.

While federal law says you can’t be billed for unexpected charges, New York law says you can’t be pushed into debt traps by the very people who are supposed to help you. The CFPB’s 2024 rule removing medical debt from credit reports is another win-but again, it only applies to debt from healthcare financing products, not regular credit cards. So even with federal protections, your payment method still determines your safety net.

That’s why New York’s rules are some of the strongest in the country. Other states are watching. If you live outside New York, ask your provider: “Do you separate consent for treatment and payment? Do you complete patient applications for financing? Do you require credit card info before emergency care?” If they hesitate, you’re not being protected.

What You Should Do Right Now

Don’t wait for a bill to arrive before you act. Here’s your checklist:

- Ask for two consent forms. One for treatment. One for payment. If they give you one, ask why.

- Never let staff fill out your financing application. Even if they say, “I’ll just help you.” Say no. Take the form. Fill it out yourself.

- Refuse to hand over your credit card before emergency care. Providers can’t legally require it. If they insist, ask to speak to a supervisor or file a complaint.

- Always read the credit card notice. If you’re paying with a Visa or Mastercard, you’re giving up legal protections. Ask if they offer a healthcare financing option instead.

- Keep copies of everything. Signed forms, notices, receipts. If a provider violates the law, you need proof.

Why This Matters Beyond New York

Medical debt isn’t a New York problem. It’s a national crisis. In 2022, 9.2% of Americans under 65 had medical debt in collections. That’s 1 in 11 people. The Urban Institute found 50.8 million Americans had medical debt in 2021. And the Kaiser Family Foundation says 74.6 million Americans have struggled with medical bills.

New York didn’t create this problem. But it’s the first state to fight it with real, enforceable rules. Other states will follow. California, Illinois, and Massachusetts are already drafting similar bills. The goal is simple: stop turning healthcare into a credit scoring game.

If you’re in New York, you have rights. If you’re anywhere else, you should demand them. Providers can’t protect you from debt unless the law forces them to. And now, for the first time, the law is on your side.

What’s Next for Patient Rights?

The suspension of Section 18-c is a red flag. It shows how fast rules can change-and how easily enforcement can stall. But the momentum is still moving. The CFPB’s 2024 rule to remove medical debt from credit reports proves federal agencies are watching. And hospitals are starting to feel the pressure.

Expect more states to adopt New York’s model: separate consent, no staff-assisted financing, no credit card holds in emergencies. The next big fight will be over transparency in pricing. Right now, you still can’t know how much an MRI will cost until after you get it. That’s changing. But only if patients keep asking.

For now, know this: you are not a debtor. You are a patient. And the law is starting to treat you like one.

Do New York’s patient protection laws apply to me if I’m not a resident?

Yes. These laws apply to any healthcare provider operating in New York State, regardless of where you live. If you receive care in New York-whether you’re visiting, working, or temporarily staying-you’re protected under these rules. The location of the provider, not your residency, determines which laws apply.

Can I still use CareCredit or similar financing plans?

Yes, but only if you apply for it yourself. Providers can’t fill out the form for you, recommend one over another, or pressure you into signing up. You’re free to choose CareCredit, CareCapital, or any other healthcare financing product-but the decision must be yours, and you must complete the application without staff assistance.

What happens if I pay with a regular credit card instead of a healthcare financing product?

You lose key legal protections. Medical debt from healthcare financing products can’t be reported to credit bureaus, can’t lead to wage garnishment, and can’t result in liens on your home under New York law. But if you use a Visa, Mastercard, or Amex, you’re treated like any other consumer debt. That means collectors can sue you, garnish your wages, and damage your credit score.

Is the suspension of Section 18-c a sign the law is being repealed?

No. The suspension means enforcement is on hold while the state clarifies how to implement it. The law still exists. Providers are still expected to follow it. The Department of Health is working on updated guidance. Until then, you should still ask for separate consent forms-it’s your right, even if providers aren’t actively enforcing it.

How do I report a provider who violates these laws?

File a complaint with the New York State Department of Health’s Office of Patient Services. You can do this online at their website or by calling 1-800-800-4820. Keep copies of all forms, receipts, and communications. The more evidence you have, the stronger your case. Violations can lead to fines of $2,000 to $5,000 per incident, so providers take these complaints seriously.

Ryan Anderson

November 13, 2025 AT 20:27I just walked out of my local ER last week because they tried to swipe my card before even checking my vitals. 🚫💉 I cited Section 519-a and they backed down immediately. New York’s laws are a godsend. If you’re getting pushed for a credit card, say NO. It’s your right.

Eleanora Keene

November 14, 2025 AT 13:31Thank you for this post. I didn’t know about the separate consent forms. I signed one big lump of paperwork after my knee surgery last year… and then got hit with a CareCredit bill I didn’t even realize I’d agreed to. 😔 I’m going back to my provider this week to ask for copies of everything. You’re right-we need to be proactive. 💪

Joe Goodrow

November 15, 2025 AT 16:35Why are we letting New York dictate healthcare policy for the whole country? This is socialist overreach. If you can’t afford care, don’t get it. Stop expecting the system to coddle you. These laws are just making providers more cautious and driving up costs for everyone else. Wake up.

Don Ablett

November 17, 2025 AT 05:27It is interesting to note that the suspension of enforcement under Section 18-c does not constitute repeal but rather a temporary pause pending regulatory clarification. One must distinguish between legal validity and administrative implementation. The underlying statutory language remains intact and enforceable by private action or complaint. This nuance is frequently misunderstood by the public

Kevin Wagner

November 19, 2025 AT 03:30Let me tell you something-this is the first time in my life I’ve felt like a human being in a hospital, not a walking ATM. I’ve been screwed over by medical debt twice. Twice. I cried reading this. If you’re reading this and you’re scared to ask for separate forms? DO IT. Walk out. File a complaint. You’re not being difficult-you’re being smart. These laws are the shield we’ve been begging for. Now use it. 🛡️❤️

gent wood

November 20, 2025 AT 10:43The distinction between healthcare financing products and traditional credit cards is profoundly significant, and I am gratified to see legislative action addressing this disparity. The absence of wage garnishment and credit reporting protections under conventional payment methods creates an inequitable burden on vulnerable populations. It is commendable that New York has taken such a principled stance. I hope other jurisdictions follow suit with equal rigor.

Dilip Patel

November 22, 2025 AT 08:43USA always make laws for show. In India we dont have any of this shit. You go to hospital, you pay cash or dont get treated. Simple. No paperwork. No rights. No drama. You think these laws help? Nah. They just make doctors more scared to treat you. I seen it. They dont want to get fined so they say no to poor people. This is why real countries dont do this.

Jane Johnson

November 22, 2025 AT 18:19Actually, the law’s suspension undermines its credibility. If enforcement is paused, then compliance is optional. This creates a legal gray zone where providers can exploit ambiguity. The very existence of this suspension suggests the law is not as robust as claimed.